Focusing on the UAE, this article explores how demand from construction and industry is shaping the powder coatings segment. It reviews certification standards, production capacities and the competitive positioning of key manufacturers, alongside broader market and supply chain trends.

Introduction

Powder coatings occupy a relatively narrow but technically important segment within the UAE’s broader industrial and construction materials market. Their role is most visible in architectural aluminium systems, industrial equipment and selected infrastructure applications, where durability, surface consistency and environmental performance are critical.

The relevance of this segment is closely linked to the scale of construction activity in the country. The UAE is undergoing a sustained expansion cycle, with the value of active and planned projects expected to exceed USD 130 billion by 2029. Demand for coated aluminium and steel is directly linked to this pipeline, particularly in civil and industrial construction, infrastructure and general industries. The construction sector is estimated to account for approximately 75% of coatings demand in the region, highlighting its central role in shaping market dynamics.

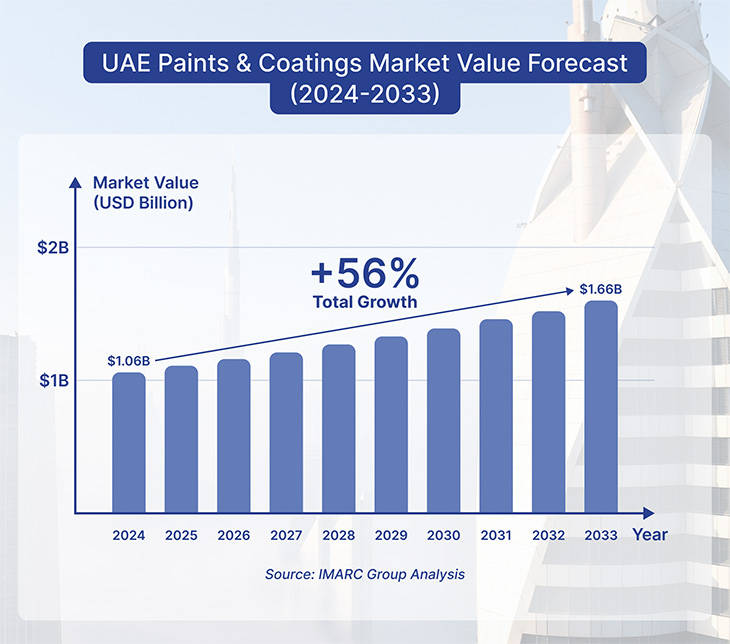

At the regional level, the Middle East paints and coatings market is estimated at approximately USD 4.5 billion, with projections reaching around USD 7.2 billion by 2030. At the same time, the UAE paints and coatings market is estimated at around USD 1.06 billion in 2024 and is projected to reach approximately USD 1.66 billion by 2033, according to IMARC Group analysis. Within this broader market, powder coatings account for a smaller share but are primarily used in applications where long-term performance and resistance to environmental stress are required. The global powder coatings market is estimated at around 11.5 billion in 2025 and is projected to reach approximately USD 18.5 billion by 2033, reflecting continued expansion of the segment, supported by demand for durable and environmentally compliant coating technologies, particularly in automotive and architectural applications.

Despite periodic geopolitical tensions affecting the wider region, construction activity in the UAE has remained relatively resilient. Market assessments, including analysis by S&P Global Ratings, indicate that project execution has broadly continued on schedule, supporting a stable demand base for industries linked to building materials and components, including coatings. This consistency not only underpins domestic consumption, but also reinforces the role of the UAE as a manufacturing platform serving regional markets.

In this context, powder coatings are best understood not simply as a finishing material, but as part of a wider industrial system connected to construction quality, industrial processing and industrial and supply-side dynamics. The manufacturing landscape in this segment includes multinational producers, regional suppliers and newer local entrants, each competing across different scales and technical capabilities. Architectural and decorative applications account for the largest share of coatings demand in the UAE, driven by ongoing real estate development and infrastructure projects.

Demand drivers, technology and competitive landscape

The global powder coatings market is driven by a combination of regulatory pressure, industrial transformation and evolving end-use demand.

Tightening environmental standards remain a key structural driver. Powder coatings, which are typically solvent-free and emit negligible levels of volatile organic compounds (VOC), are increasingly replacing liquid coatings across multiple industries. Regulatory developments in major markets, including carbon-related mechanisms in the European Union and sustainability-focused policies in China, are accelerating this transition.

Demand is also expanding across core industrial sectors. The shift toward electric mobility is creating new applications for high-performance coatings, particularly in battery systems and structural components. At the same time, large-scale construction activity and giga-projects in the Middle East - including in Saudi Arabia and the UAE - continue to support demand for aluminium-based applications requiring durability, corrosion resistance and UV stability.

Technological advancements are further expanding the market. Low-temperature curing systems enable application on heat-sensitive substrates, while advanced formulations improve corrosion resistance and overall performance, opening new use cases in furniture, electronics and industrial segments.

Regional conditions also play a defining role. In the Gulf, high UV exposure, humidity and salinity increase the importance of long-life coating systems and higher-specification materials.

Against this backdrop, the competitive landscape remains relatively consolidated, with global players such as AkzoNobel, Axalta Coating Systems, PPG Industries, Sherwin-Williams, Jotun and Hempel maintaining strong positions across regions.

Recent corporate disclosures illustrate both scale and consolidation trends. Sherwin-Williams reported revenue of approximately $23.6 billion, while Axalta Coating Systems generated just over $5 billion, reflecting its position as a global coatings specialist. Jotun has also demonstrated continued growth in powder coatings, supported by demand across the Middle East, Southeast Asia and Europe. A recently announced combination involving AkzoNobel and Axalta Coating Systems, expected to be completed in 2026–2027, would create a combined entity with an estimated market capitalisation of around $25 billion and projected revenues of approximately $17 billion.

Industry consolidation is expected to continue, with potential large-scale combinations among major players reinforcing the importance of scale, global supply capabilities and integrated product portfolios.

Standards, climate and technical requirements in the Gulf

Powder coatings in the UAE operate under some of the most demanding climatic conditions globally. High levels of solar radiation, constant UV exposure, elevated temperatures, humidity and coastal salinity create a combination of stress factors that directly affect coating durability, particularly in architectural applications.

In this environment, performance requirements extend well beyond standard benchmarks. Certification systems such as QUALICOAT serve as a key reference point for the market, defining requirements for raw materials, production processes and finished coating performance. QUALICOAT Class 1 and Class 2 are widely used in architectural aluminium applications, while higher-performance specifications are applied in projects requiring extended durability.

Across the UAE market, several manufacturers hold internationally recognised certifications such as Qualisteelcoat and QUALICOAT, including AkzoNobel, Axalta Coating Systems, Qemtex Powder Coatings, Jotun, PPG Industries and other other regional suppliers.

However, certification alone does not guarantee performance in Gulf conditions. In practice, durability depends on consistent control across formulation, surface pretreatment and curing, as even minor deviations can lead to accelerated degradation under exposure to UV, heat and salinity.

Access to suitable raw materials is also a key factor. Polyester resins, pigments and additives designed for UV and chemical resistance are critical for achieving stable performance. This places additional importance on supply chain reliability, particularly in a market where disruptions to international logistics can affect both cost and availability of inputs.

At the formulation level, polyester-based powder coatings dominate architectural applications due to their superior resistance to UV exposure and weathering, particularly in environments with prolonged solar radiation. Industry data indicates that polyester systems account for a significant share of the market and are widely used in aluminium and other outdoor applications requiring long-term durability. Alternative chemistries such as epoxies and hybrids are typically limited to interior or less exposed environments due to lower resistance to sustained UV exposure.

Major manufacturers, capacities and market structure in the UAE

The UAE powder coatings market is relatively concentrated, with a limited number of established manufacturers accounting for the majority of specification-driven demand, particularly in architectural applications.

At the top tier of the market, Jotun and AkzoNobel represent the most established international players with long-term production footprints in the UAE. Jotun has developed one of the earliest manufacturing platforms in the UAE and is currently expanding its industrial base through the construction of a new facility in Abu Dhabi valued at approximately AED 450 million, with a total area of over 83,000 square metres, replacing its existing site.

AkzoNobel operates a dedicated powder coatings manufacturing facility in Dubai, supporting architectural and industrial applications across the UAE and export markets. The company is also developing a colour mixing and distribution centre for aerospace coatings in Dubai, expected to become operational in 2026, adding to its regional production and supply infrastructure.

Axalta Coating Systems represents a later entrant into local manufacturing, having established its UAE production base through the acquisition of Capital Paints in Ras Al Khaimah in 2019. While detailed production volumes are not publicly disclosed, the facility focuses on thermosetting powder coatings, particularly for architectural applications, and forms part of Axalta’s broader regional manufacturing network.

A recent addition to the UAE powder coatings manufacturing landscape is Qemtex, which commissioned its production facility in Umm Al Quwain in 2024. The plant was launched with an initial capacity of approximately 5,000 tonnes per year, with infrastructure designed to support expansion to around 10,000 tonnes, backed by an investment of around USD 16 million.

National Paints Factories Co. Ltd. operates a large-scale manufacturing complex in Sharjah, with an estimated area of around 130,000 square metres and multiple integrated production lines. In 2025, the company reported production of approximately 264 million litres, including powder coatings, and generated sales of around USD 537 million. Its operations form part of a broader manufacturing network spanning multiple countries.

Taken together, the market can be described as concentrated but evolving, with established manufacturers maintaining strong positions alongside growing local production capacity and increasing competitive activity.

Based on disclosed capacities and available industry data, total powder coatings production capacity in the UAE can be estimated in the range of 22,000–30,000 tonnes annually, indicating a relatively concentrated market structure dominated by a limited number of mid- to large-scale producers.

Outlook and development scenarios for the UAE powder coatings market

Looking ahead, the development of the UAE powder coatings market is expected to remain closely linked to broader industrial and economic dynamics. As coatings are integrated across key sectors such as construction, manufacturing, transport and energy, market activity will depend on the pace of industrial expansion and infrastructure investment. In this context, continued economic diversification and the development of non-oil industries are likely to shape demand patterns. At the same time, project specifications and technical requirements are expected to influence material selection and supply structure.

At the global level, powder coatings production is expected to continue expanding, with volumes projected to grow from approximately 4.4 million tonnes in 2024 to around 5.5 million tonnes by 2028.

Recent disruptions in key trade routes have exposed the vulnerability of supply chains for imported raw materials and finished products. This has increased pressure on manufacturers to ensure supply reliability, particularly in projects where timing and specification compliance are critical.

At the same time, the combination of harsh climate exposure and strict certification requirements raises the bar for performance. In practice, competition is shaped less by price alone and more by the ability to deliver consistent quality under real condition.

In this context, local manufacturing is becoming a structural advantage. Production within the UAE allows for shorter lead times, greater flexibility in meeting project requirements and tighter control over quality. Recent capacity expansions and the entry of new production platforms suggest that this shift is already underway.

Overall, the market is gradually moving toward a model where reliability, technical performance and supply responsiveness define competitive positioning. Manufacturers that can consistently meet these requirements are likely to strengthen their position, particularly in architectural and other specification-driven segments.